14

ANNUAL REPORT 2015

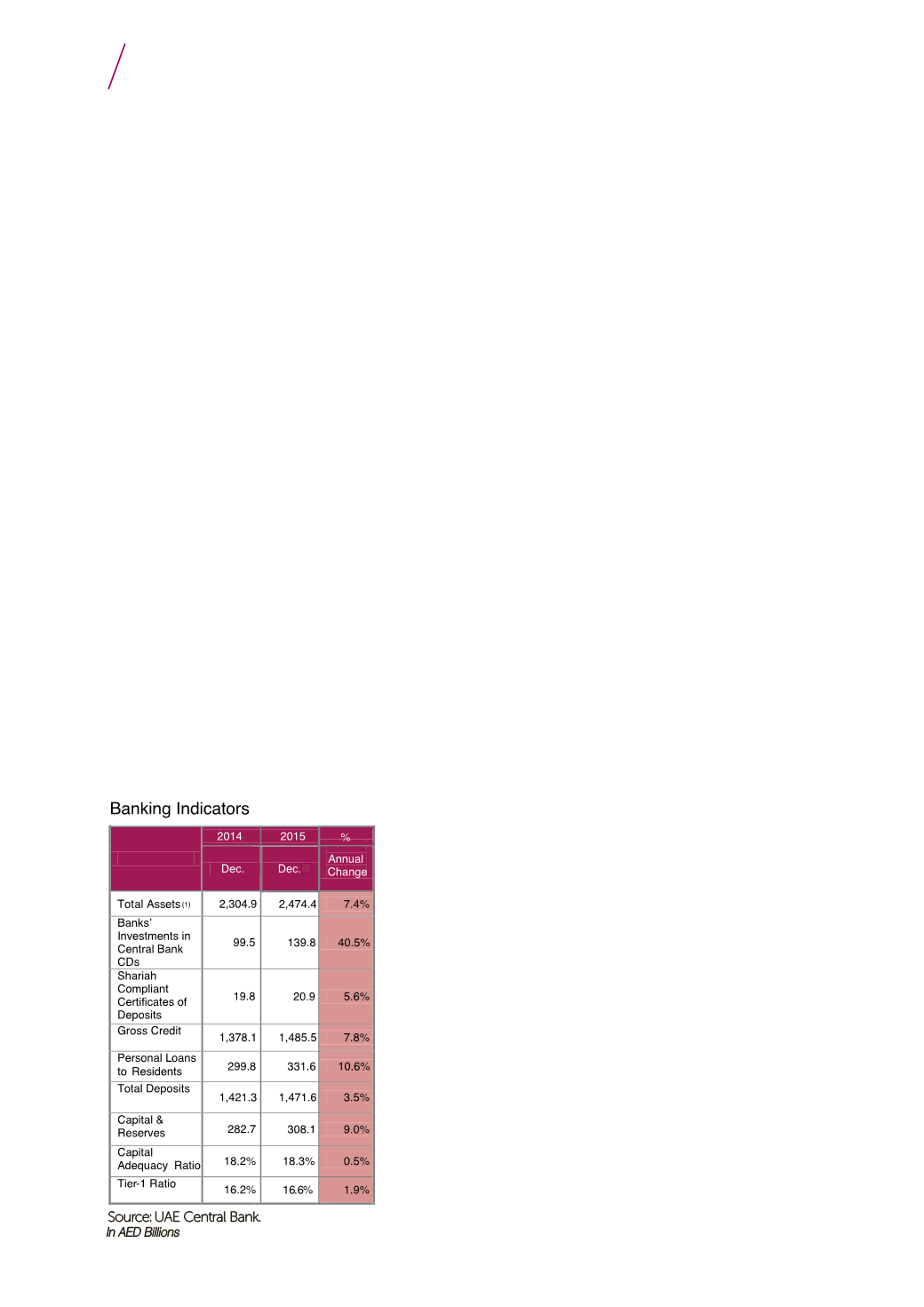

BANKING & MONETARY DEVELOPMENTS

Stable Outlook

. The ratings agency believes UAE

banks' credit profiles will broadly remain resilient

despite an economic slowdown driven by low

oil prices.

Return on assets is likely to remain at around

two per cent, while profitability should remain

stable, supported by solid margins, stable

operating costs and provisioning charges.

Moody’s also noted that capital buffers are

solid and expects them to improve further, with

tangible common equity expected to reach

around 15 per cent of risk-weighted assets in

2016, up from around 13.8 per cent in 2015.

However, in line with tightening liquidity across

the GCC region as a result of lower oil prices,

liquidity metrics for UAE banks may decline for the

first time since the 2008 crisis. Liquid assets are

expected to decline to a still solid 25 per cent in

2015 from a peak of around 30 per cent of total

assets in December 2014.

The softening economy will affect operating

conditions and result in subdued credit growth.

Moody’s predicts credit growth to slow down to

three to five per cent annually for 2015 and 2016

from around nine per cent for 2014. Asset quality

should remain stable, with impairments at around

five per cent of total loans for 2016.

Although funding costs are increasing,

Moody’s expects that it will largely be offset by

rising corporate yields, as US-linked interest rates

increase and the ratings agency expects highly

competitive lending pressures to ease into 2016.

Deposit growth decelerated sharply in 2015,

a factor that will continue into 2016 to two to

four per cent from 10 per cent in 2014. This has

resulted in banks raising funds through bonds

and Sukuk issuance to support growth.

Moody’s forecasts real GDP growth of around

3.1 and 3.2 per cent for 2015 and 2016, down

from 4.6 per cent in 2014, stating that the UAE

economy remains the most diversified in the

region with continued public-sector spending

by the Emirate of Abu Dhabi complementing

continued growth in Dubai's diversified private

sector, specifically in trade and transport.

Nevertheless, the impact of prolonged low

oil prices on the UAE's economy will slow credit

growth to three to five per cent on an annual basis,

down from around nine per cent in 2014. Moody’s

cautions that intensification of geopolitical

tensions in the region and the prospect of a more

protracted period of low oil prices would dampen

confidence, future spending and economic growth.

Credit

An easing in the appetite for credit was evident

through almost all sectors of the economy as

2015 progressed and the oil price continued

to fall. At the same time, and especially

through the latter part of the year, there was

a tightening of credit standards. This reflected

a reduced willingness to extend business

loans and a rising degree of risk aversion.

Collateralisation requirements and premiums

charged on riskier loans tightened through the

year as did conditions on the maximum size of

credit lines and spreads over the cost of funds.

An improvement in the quality of the loan

portfolio of banks, ascribed by some as partly

due to expanding operations of Al Etihad

Credit Bureau, may be seen in the fall in the

ratio of NPLs from a peak of seven per cent at

end-2014 to 6.3 per cent at end-2015. Over

the first half of 2015 bank specific provisions

for NPLs dropped from the peak recorded

in November 2014 of AED 91.1 billion

but increased marginally in the second

half of 2015.

The Central Bank of United Arab Emirates’

Credit Sentiment Survey

highlighted a down-

tick in credit appetite towards the end of the

year. This contraction in Q4 2015 followed

several quarters of robust lending growth but

concerns that Iran may oversupply the market

with oil, further undermining the price, and